Medicare Supplement Plans (Medigap)

Medicare Supplement plans—also known as Medigap—are offered by private insurance companies to help cover many of the out-of-pocket costs that Original Medicare (Parts A and B) does not pay.

With Original Medicare, Medicare typically pays its portion of approved medical expenses first. Your Medicare Supplement plan then helps cover some or most of the remaining costs, depending on the specific plan you choose.

What do Medicare Supplements Cover?

Original Medicare generally covers about 80% of approved Part B services, leaving you responsible for the remaining 20% with no cap on your out-of-pocket costs.

A Medicare Supplement plan is designed to help reduce—or in some cases eliminate—those remaining expenses. Depending on the plan, coverage may include:

• Part A hospital deductible

• Part B coinsurance (the 20%)

• Skilled nursing facility coinsurance

• Hospice coinsurance

• Foreign travel emergency (on select plans)

This can provide significant financial predictability, especially for those who want more consistent healthcare costs.

What Medicare Supplements Do Not Cover

Medigap plans do not include coverage for:

• Routine dental, vision, or hearing exams

• Hearing aids

• Eyeglasses or contact lenses

• Long-term care or custodial care

• Retail prescription drug coverage (Part D is separate)

Plan Options

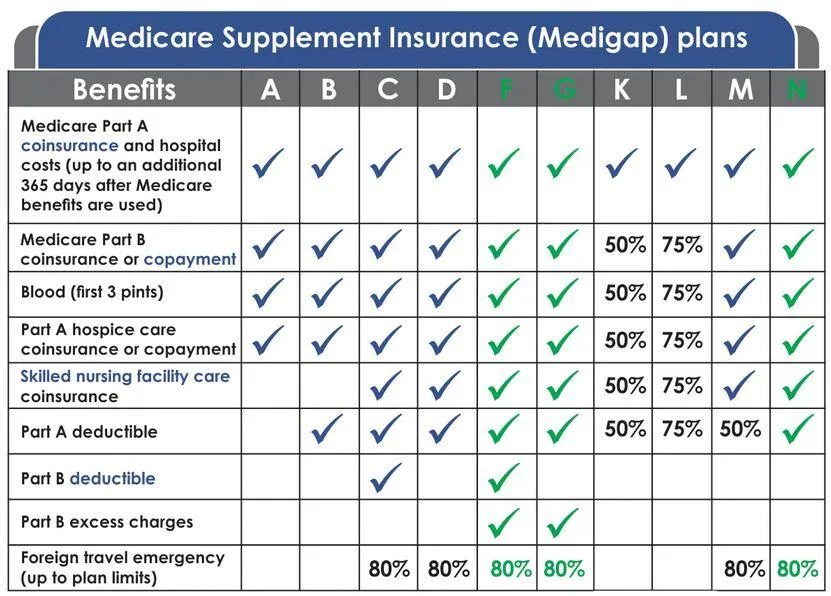

Medicare Supplement plans are standardized and labeled by letters (such as Plan G, Plan N, etc.), with each plan offering a different level of coverage. This allows you to choose a plan that aligns with your healthcare needs and budget.

Plans that are highlighted in green above are the 3 most popular plans that clients choose when selecting a Medigap/Medicare Supplement plan.

Get a Consultation

& Quote at No Cost

Have any questions?

Phone: 470-934-2122

© MedCovPro LLC. All Rights Reserved.

Contact

FAQ

Privacy Policy